By Ada Walker| Macro & Markets | 2024 Outlook

Entering 2024: Inflation Still Lingers

As 2024 begins, global markets are gripped by one question: has inflation truly been tamed, or will central banks need to keep rates higher for longer?

Despite rapid tightening cycles in 2022–2023, price pressures have proven stubborn. In the U.S., inflation cooled sharply from its 9% peak in 2022 but remained above the Federal Reserve’s 2% target entering 2024. Core services — particularly housing and labor-intensive sectors — continued to show resilience.

This stickiness reignited debate within the Fed and among investors about whether rate cuts in 2024 are premature, or whether the “higher-for-longer” era has only just begun.

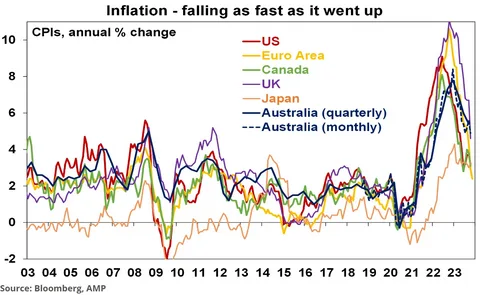

Inflation’s Mixed Signals

- Headline CPI (late 2023): Settled near 3%, down from 6.5% at the start of the year, largely due to cooling energy and goods prices.

- Core CPI and Core PCE: Still running at 3.5–4%, driven by rents, healthcare, and wage-linked services.

- Wages: Annual growth around 4% YoY, outpacing productivity gains, sustaining fears of a wage–price spiral in select sectors.

These dynamics left policymakers cautious: progress was undeniable, but the “last mile” toward 2% inflation looked far harder than the initial drop.

Fed Caught Between Growth and Prices

At its December 2023 meeting, the Fed signaled the possibility of three rate cuts in 2024, sparking a rally in equities and a drop in the dollar. Yet not all officials were convinced. Hawks warned that loosening too soon could undo disinflation progress.

By early 2024, two camps emerged:

- The Doves: Argued that slowing job growth, softer retail sales, and weaker housing demand justified gradual easing.

- The Hawks: Pointed to sticky core inflation and resilient wages as reasons to keep rates elevated through much of 2024.

The result? A policy outlook clouded with uncertainty, forcing investors to hedge both scenarios.

Higher-for-Longer in Global Context

The debate wasn’t unique to Washington.

- European Central Bank: After hiking aggressively, the ECB faced similar dilemmas: inflation moderated but wage settlements kept price growth elevated.

- Bank of England: Continued to stress vigilance, with services inflation above 5%.

- Bank of Japan: Still held ultra-loose settings, but speculation about policy normalization gathered pace as core prices stayed firm.

This divergence created volatile cross-currency dynamics, with the U.S. dollar oscillating as markets weighed Fed cuts against relatively cautious peers.

Market Reaction: Rates, Bonds, and the Dollar

Bond markets captured the tug-of-war.

- Treasury yields: After peaking near 5% in 2023, the 10-year yield slid toward 4% on cut expectations, before rebounding on sticky inflation prints in early 2024.

- Dollar: The U.S. Dollar Index (DXY) pulled back in late 2023 but remained supported by relative U.S. strength and global risk aversion.

- Equities: U.S. stocks rallied on the prospect of lower rates but stayed vulnerable to inflation surprises.

Investors learned quickly that each CPI release could swing sentiment dramatically — one hot print was enough to revive higher-for-longer bets.

Risks to Watch

- Labor Market Resilience – If unemployment stays below 4% and wage growth above 4%, inflation could prove more entrenched than expected.

- Housing & Services – Shelter costs, sticky in 2023, may continue to feed into core CPI.

- Geopolitical Shocks – Energy markets remain sensitive to supply disruptions; another spike could derail disinflation trends.

- Policy Credibility – Cutting too soon risks unanchoring expectations; waiting too long risks recession.

Lessons from the Last Cycle

The Fed’s cautious pivot highlighted a key reality: once inflation expectations reset upward, credibility is hard to reclaim. Policymakers now prize stability over speed, preferring to err on the side of tightness rather than reignite another wave of price growth.

Markets, meanwhile, must navigate a world where the Fed is no longer an automatic source of cheap liquidity. The higher-for-longer narrative may keep borrowing costs elevated, corporate margins pressured, and emerging markets under stress.

Conclusion

2024’s story is not just about whether inflation falls — but how fast, and whether central banks dare to ease before the job is done. For now, the debate continues: doves see room for cuts, hawks warn of stickiness, and markets remain caught in between.

One lesson is clear: after years of ultra-low rates, the “higher-for-longer” world is here, and investors must adapt to a new reality where inflation’s persistence keeps central banks on edge.