Introduction

The United States dollar began the week on a cautious note, slipping against major currencies as traders weighed the twin risks of a potential government shutdown and upcoming economic data releases. Investors had previously relied on the greenback as a safe haven, supported by resilient U.S. growth and speculation about delayed rate cuts from the Federal Reserve. However, the combination of fiscal uncertainty, weaker confidence in long-term debt sustainability, and shifting capital flows has added fresh pressure. With nonfarm payrolls and inflation readings due later in the week, the dollar’s short-term outlook remains clouded by both domestic politics and global economic forces.

Global Dollar Performance

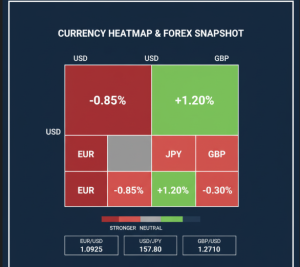

The U.S. Dollar Index (DXY) declined around 0.2 percent on Monday, pulling back from resistance levels near 98.50. The euro strengthened modestly, climbing above 1.1720, while the Japanese yen regained some ground, trading around 149.80 per dollar. Analysts highlighted that the recent weakness does not erase the dollar’s broader strength. In September, the dollar continued to post gains against a basket of currencies, as U.S. Treasury yields remained elevated and global demand for dollar liquidity persisted.

Spotlight on Emerging Markets

Emerging market currencies remain under acute pressure from U.S. monetary dynamics. Indonesia drew headlines when state banks announced plans to raise U.S. dollar deposit rates to attract liquidity. The finance ministry quickly clarified that the government had not mandated such a move, raising questions about institutional coordination and confidence. The announcement sparked volatility in the rupiah, reminding traders that emerging markets remain vulnerable to fluctuations in U.S. funding conditions.

In Latin America, Argentina entered negotiations with the United States for a potential 20 billion dollar swap line to stabilize its reserves. While such support could provide breathing space, it underscores how dependent some economies remain on access to dollar liquidity during times of stress.

Federal Reserve and Interest Rate Expectations

The Federal Reserve’s policy path continues to dominate currency markets. While investors had initially priced in aggressive rate cuts by the end of the year, strong U.S. data and hawkish commentary from Fed officials have tempered those expectations. Chair Jerome Powell recently emphasized a cautious and data-driven approach, which markets interpreted as a signal that near-term easing will likely be slower than previously expected.

Traders are now watching closely for any sign that labor market data or core inflation figures will shift the Fed’s timeline. If payrolls remain strong and inflation fails to moderate, the central bank may hold rates higher for longer, giving the dollar renewed support.

Fiscal Pressures and Debt Concerns

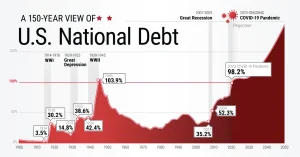

Beyond monetary policy, fiscal dynamics are adding to the uncertainty. The United States national debt recently crossed the 35 trillion dollar threshold, with annual deficits showing no signs of narrowing. Economists warn that persistent fiscal imbalances erode long-term confidence in the dollar, particularly if foreign demand for U.S. Treasuries weakens.

The immediate risk is the possibility of a federal government shutdown if Congress fails to pass funding legislation. Such a disruption could delay the release of economic data, undermine investor confidence, and create near-term volatility. In past episodes, shutdowns have often led to short-lived dollar weakness, though the longer-term impact depends on the severity and duration.

Global Capital Flows and Safe Haven Dynamics

Despite headwinds, the dollar remains the world’s most reliable safe haven. During periods of geopolitical stress or financial turbulence, global capital tends to flow back into U.S. assets. This dynamic has cushioned the dollar’s decline and explains why losses remain limited.

At the same time, traders are increasingly considering diversification strategies. Some institutional investors are allocating small portions of their portfolios to non-traditional hedges, ranging from commodity baskets to select digital settlement tools. While these moves are still peripheral, they reflect a cautious interest in reducing reliance on the dollar’s dominance in every scenario.

Subtle Counter Narrative: Alternative Assets

The debate over the long-term future of the dollar often surfaces in quieter corners of the market. Some traders highlight the gradual emergence of alternative assets that may act as hedges against U.S. currency volatility. These are not replacing the dollar but serve as insurance in portfolios that seek resilience. Observers note that digital frameworks designed for programmable settlement and cross-border transactions are receiving attention in policy discussions, even if their adoption remains limited today. Such developments are not yet mainstream but indicate that the conversation about diversification is broadening.

Market Implications and Outlook

The immediate drivers of the dollar this week will be the nonfarm payrolls report, the core personal consumption expenditures index, and congressional negotiations over funding. If economic data surprises to the upside while a shutdown is avoided, the dollar could rebound strongly. Conversely, weak data combined with political gridlock may deepen near-term weakness.

For technical traders, support levels near 97.80 on the Dollar Index are critical. A break below could open the path toward 97.20, while resistance around 98.60 remains the ceiling to watch. In cross-currency terms, EUR/USD could extend toward 1.1780 if momentum persists, while USD/JPY may retest 150.50 if risk aversion returns.

Conclusion

The United States dollar faces a complex environment shaped by fiscal politics, monetary policy uncertainty, and global capital flows. While near-term weakness has emerged, the greenback’s role as the world’s dominant reserve currency continues to provide resilience. For traders and analysts, the challenge lies in balancing confidence in the dollar’s safe haven status with awareness of structural vulnerabilities. The coming week will serve as an important test of both the short-term trend and the long-term narratives shaping the currency landscape.